In our recent piece on construction types, we showed how core building decisions shape insurance exposure.

This is the next layer: how design strategy, building systems, and loss prevention measures can further affect deductibles, underwriting, and NOI.

Most developers still treat insurance as a downstream cost.

In reality, it is being shaped much earlier.

Construction type remains one of the first things insurers evaluate. But it is not the only one.

Water protection, fire resilience, system visibility, access control, and ongoing building condition all help shape how risk is viewed and priced.

That is already showing up in real numbers.

- In one multifamily case cited by Multi-Housing News, a 50-story community reduced its water-damage deductible from $2 million to $100,000 after installing leak detection.

- Leak detection and shutoff systems can also reduce claim frequency by up to 96% and severity by about 72%, according to LexisNexis Risk Solutions.

Those are not small operational improvements. They are underwriting signals.

What Insurers are Pricing

Insurers consistently look at a few core drivers:

- Construction type

- Fire protection systems

- Location and exposure

- Occupancy and use

- Building systems and condition

For developers, the key point is this: several of these factors are heavily influenced by design and engineering decisions made early in the project.

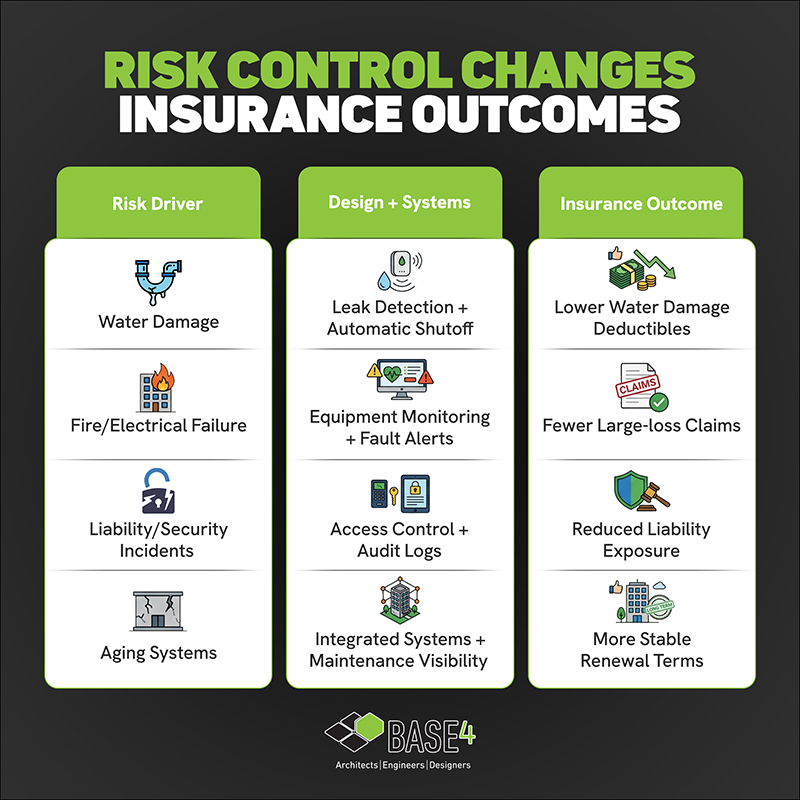

How Design Decisions Change Insurance Outcomes

The design response matters because it can reduce both the likelihood and severity of loss.

- Water damage: Leak detection and automatic shutoff can reduce water-loss severity and deductible exposure.

- Fire and electrical failure: Monitoring and fault alerts can reduce system failures before they become large-loss events.

- Liability and security incidents: Access control, lighting, and better site visibility can reduce liability exposure.

- Aging systems: Integrated systems and maintenance visibility can improve long-term building performance and renewal profile.

Why This Matters Financially

For developers and owners, the business impact is straightforward:

- Lower deductibles mean less capital exposed per loss event

- Better risk controls can support stronger underwriting

- Fewer large losses can help stabilize premiums over time

- Lower volatility helps protect NOI

Insurance is not just reacting to the building after the fact. It is increasingly responding to what the design makes possible.

Why Acting Early Matters

Many of the most insurance-sensitive decisions are made before the project team thinks of them that way.

Once major design decisions are set, these improvements are often more expensive, more disruptive, and less effective to implement.

The advantage comes from addressing them in concept, not after design development.

How BASE4 Helps

BASE4 addresses insurability early by coordinating architecture, structure, and MEP around risk-sensitive design decisions.

That includes:

- evaluating insurance-sensitive design choices earlier in the process

- coordinating systems that reduce loss exposure

- helping teams think beyond first cost to long-term operating performance

For developers, that can mean a project that is better positioned for underwriting, more operationally resilient, and less exposed to avoidable insurance-related cost pressure.

If you want to evaluate a project’s insurance exposure early, BASE4 can help identify the design decisions most likely to affect deductibles, underwriting, and long-term operating risk.

Thank you,

Blair Hildahl

BASE4 Principal

608.304.5228

BlairH@base-4.com

![]()